robotics-markets

The $150 Billion Nervous System: Why Middleware is the Real Robotics Gold Rush

ABI Research's $150B forecast reveals the real value in the physical AI decade won't be captured by whoever builds the smartest model, but by whoever builds the enterprise middleware that makes models actually deployable.

By Daniel Osei, Financial Analysis · July 6, 2026 · 9 min read

Architectural diagram of a robotics middleware stack, showing the layers between foundation models and physical robot hardware

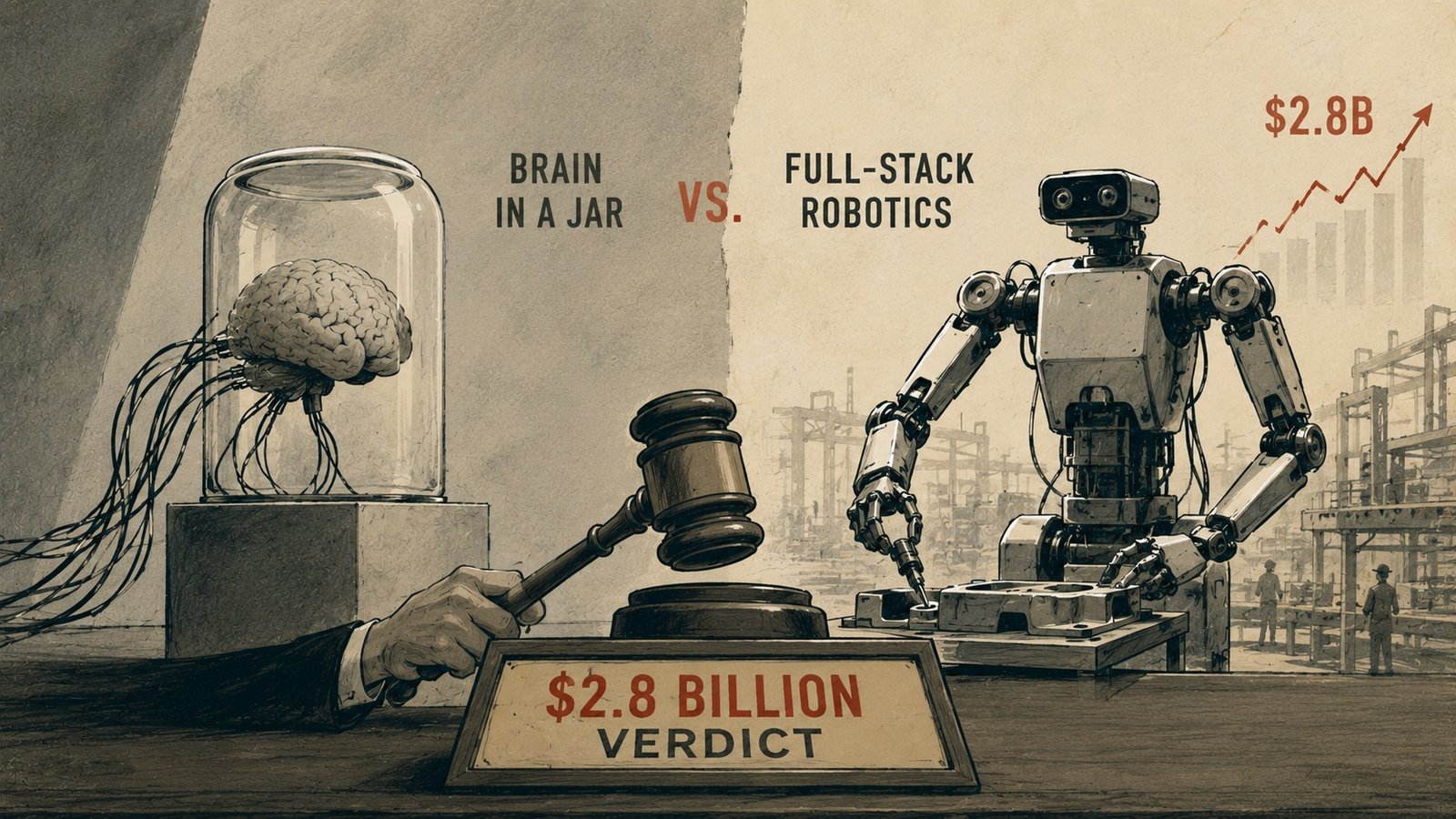

The release of ABI Research’s latest report this past week, forecasting a $150 billion market for robotics foundation models by 2036, is grabbing headlines for its sheer scale. But looking past the top-line number reveals a much more profound market reality. The true economic value of the next decade of robotics will not be captured by the companies building the smartest "brains." It will be captured by the companies building the "nervous system."

While the venture ecosystem remains fixated on model innovation, funding the next great Vision-Language-Action (VLA) architecture, the actual bottleneck to industrial deployment is system orchestration. A foundation model is mathematically brilliant, but functionally inert. To do actual work, it requires an enterprise-grade ecosystem of deterministic middleware, edge deployment infrastructure, and real-time fleet management.

The Brain is Commoditizing; The Nervous System is Not

We are rapidly approaching a reality where highly capable foundation models are table stakes. Whether an enterprise is deploying humanoid robots, mobile manipulators, or autonomous forklifts, the core intelligence layer will likely be powered by a handful of dominant models.

But a model is just a massive matrix of weights. It does not natively know how to interface with a proprietary industrial controller. It does not know how to handle an over-the-air (OTA) update while a robot is mid-task. It does not know how to seamlessly hand off a telemetry stream from a local edge node back to a central facility when a failure state occurs.

These are not AI problems; they are distributed systems problems. And right now, the industry is woefully under-equipped to solve them.

The Necessity of Deterministic Edge Execution

Currently, many robotics startups are attempting to run physical deployments on fragile, ad-hoc software stacks. They treat the robot as an endpoint for a cloud API. This approach is fundamentally incompatible with the physics of the factory floor.

When a physical machine is operating alongside human workers, action execution must be deterministic. The latency between perception and actuation cannot fluctuate based on server load. This mandates a hard shift away from cloud-dependent SaaS wrappers toward local-first, native edge execution.

The multi-billion dollar opportunity highlighted by ABI Research lies in building the middleware that guarantees this deterministic execution. We need a robust hardware interface layer that sits between the VLA model and the physical actuators, a system that translates the model’s semantic intent into microsecond-accurate torque commands while continuously monitoring the local hardware state without ever pinging a remote server.

Orchestration at Fleet Scale

The complexity multiplies exponentially when moving from a single impressive prototype to a fleet of 500 active units.

Who builds the Kubernetes for physical AI? Managing a fleet of autonomous robots requires an orchestration layer capable of handling massive streams of multimodal data in real-time. This "nervous system" must manage predictive maintenance scheduling, coordinate spatial routing across heterogeneous fleets (e.g., standard robotic arms working alongside mobile bases), and securely deploy fine-tuned model weights to edge devices without interrupting the manufacturing cycle.

The Invisible Infrastructure

The history of technology suggests that the biggest winners of a paradigm shift are rarely the ones who build the most visible applications; they are the ones who supply the infrastructure. In the PC era, it was the operating system. In the cloud era, it was the virtualization and orchestration layers.

In the physical AI era, the crown jewel will be the orchestration and edge deployment ecosystem. While the world watches the robots, the smartest money is looking at the invisible nervous system that makes them move. The race to $150 billion won't be won by the most elegant algorithm, but by the most resilient middleware.

More From Robotics Weekly

Part of Issue 4: Who Owns the Stack, published July 6, 2026→